Who This Guide Is For

In January 2022, an investor with a 20% TQQQ / 80% SPY portfolio had watched that TQQQ position grow from $100,000 to $183,000 over the previous year - quietly drifting from 20% to 26% of the portfolio without triggering any action. When TQQQ fell 79% in 2022, that extra 6% allocation cost them an additional $10,980 in losses beyond what their original risk budget intended. Not because the strategy failed. Because no one set a rule for when to trim.

This guide is about that rule: when to rebalance a portfolio containing leveraged ETFs, how to set the thresholds, what the research says about frequency, and how tax treatment shapes the practical decision.

If you are new to leveraged ETFs, read the TQQQ guide first. Rebalancing decisions only make sense once you understand what daily leverage reset does to a portfolio over time.

Bottom Line

Rebalancing a portfolio containing leveraged ETFs is not the same as rebalancing a standard equity portfolio. The daily internal reset of a 3x fund means the fund itself manages its own leverage ratio - what you are rebalancing is your allocation to the leveraged position relative to the rest of the portfolio.

The research is clear on two points. First, calendar-based rebalancing (quarterly, annually) is inferior to threshold-based rebalancing for portfolios with high-volatility components - verified by Hsieh, Chang, and Chen (arXiv:2504.20116, April 2025), Pauchlyova/Quantpedia (November 2025), and Vanguard’s threshold rebalancing research (Zhang et al., December 2024). Second, the commonly cited “rebalance drag” from daily leverage reset is a myth - variance drain comes from the volatility of the underlying, not from rebalancing frequency. Changing how often you rebalance does not fix volatility decay.

What rebalancing does control: concentration risk as leveraged ETF positions grow, and the allocation drift that turns a 20% TQQQ position into a 45% one after a bull run.

The Myth That Needs to Die First: Rebalance Drag

Before any discussion of strategy, one widely repeated claim needs to be corrected.

Many retail investors believe that rebalancing a leveraged ETF more frequently reduces volatility decay. The logic seems intuitive: if the fund resets daily and that causes decay, rebalancing more often must help. It does not.

Volatility decay - also called variance drain or beta slippage - is a function of the squared daily volatility of the underlying index multiplied by the leverage factor. The formula:

Decay ≈ L × (L-1)/2 × σ²

Where L = leverage multiple and σ² = variance of daily returns.

As ReturnStacked’s analysis (March 2025) makes explicit: compounding does not respond to rebalancing frequency - it responds to the volatility of the underlying returns. Even with monthly or quarterly rebalancing of your allocation to the leveraged ETF, the internal decay mechanism inside the fund continues at the same rate. You cannot reduce volatility decay by changing how often you rebalance your portfolio.

What you can change by rebalancing: your concentration in the leveraged position, your risk exposure relative to your original target, and the tax timing of realized gains.

What Rebalancing Actually Does in a Leveraged ETF Portfolio

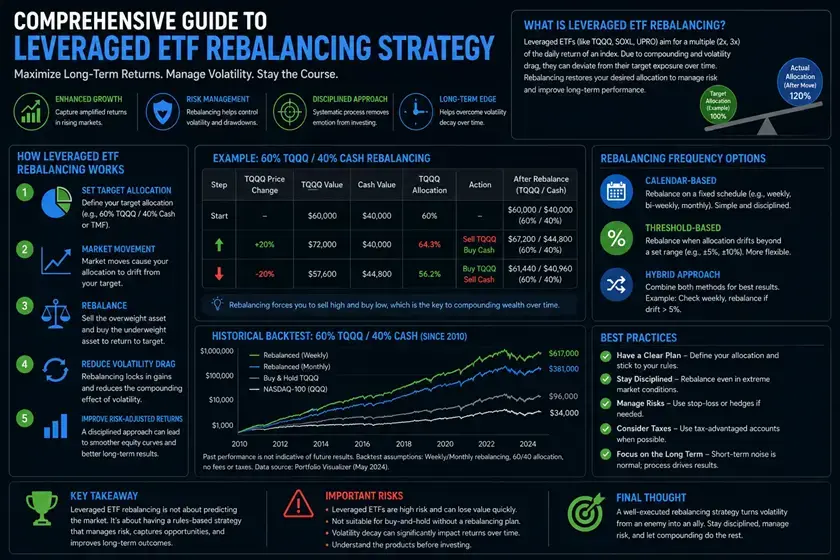

Rebalancing in this context means restoring your target allocation between the leveraged ETF and the rest of your portfolio - typically a mix of unleveraged equity, bonds, or cash.

Consider a portfolio with a 20% TQQQ / 80% SPY target allocation and $500,000 in total assets:

- TQQQ position: $100,000

- SPY position: $400,000

After a strong bull year where TQQQ returns +83% (as in 2021) and SPY returns +28.7%:

- TQQQ: $100,000 × 1.83 = $183,000

- SPY: $400,000 × 1.287 = $514,800

- Total: $697,800

- New TQQQ allocation: $183,000 / $697,800 = 26.2%

Without rebalancing, a 20% target has drifted to 26.2% - a 31% relative increase in leveraged exposure. In a subsequent down year, this larger TQQQ position amplifies losses beyond what the original risk budget intended.

Rebalancing restores the 20% target: sell $43,440 of TQQQ, buy $43,440 of SPY. This is not about improving returns - it is about keeping risk at the level you chose, not the level that drift created.

Calendar Rebalancing vs. Threshold Rebalancing

Two primary approaches exist for deciding when to rebalance.

Calendar Rebalancing

Rebalance on a fixed schedule - monthly, quarterly, or annually - regardless of how much the allocation has drifted. Simple to implement, easy to automate.

The problem: in a portfolio containing a 3x leveraged ETF, calendar rebalancing can trigger unnecessary transactions during periods of low drift, and fail to rebalance during periods of rapid drift. A leveraged ETF position can move 15-20% in a single week during volatile markets. A quarterly schedule may mean the position is significantly overweight for months before the rebalancing date.

HFEA (Hedgefundie’s Excellent Adventure) originally called for quarterly rebalancing of the 55/45 UPRO/TMF combination. The strategy’s Bogleheads thread generated extensive discussion of whether monthly or quarterly was superior - the conclusion was that the difference was small for that specific two-fund portfolio, but that threshold-based variants consistently produced better outcomes in backtests.

Threshold Rebalancing

Rebalance when the allocation to any position drifts beyond a defined band from the target, regardless of calendar timing.

BBH’s framework (Justin Reed, “Our Approach to Portfolio Rebalancing for Taxable Investors,” April 30, 2025) recommends an absolute band of ±5% at the major asset class level and a relative band of ±25% at the sub-asset class level. Applied to a leveraged ETF position:

- Target: 20% TQQQ

- Absolute band: rebalance when TQQQ reaches 25% or falls to 15%

- Relative band: rebalance when TQQQ reaches 25% (20% × 1.25) or 15% (20% × 0.75)

In this case both methods produce the same trigger points - a common outcome when the target allocation is 20%.

The arxiv.org research paper on LETF rebalancing - Hsieh, Chang, and Chen, “Compounding Effects in Leveraged ETFs: Beyond the Volatility Drag Paradigm,” arXiv:2504.20116, April 2025 - found that daily-rebalanced LETFs are optimal in momentum markets, while less frequent rebalancing reduces losses in mean-reverting conditions. The practical takeaway: there is no single optimal rebalancing frequency. The right approach depends on current market regime - which investors cannot reliably identify in advance. Threshold-based rebalancing sidesteps this by responding to actual drift rather than calendar assumptions about market behavior.

Setting the Right Threshold Bands

For a portfolio containing a leveraged ETF, the appropriate threshold bands are wider than for a standard equity portfolio. The reason: transaction costs and tax events from rebalancing too frequently can exceed the benefit of tighter allocation control.

For a 10-20% leveraged ETF allocation: A relative band of ±25-30% is appropriate. This means a 15% target triggers rebalancing at 19.5% or 10.5%. A 20% target triggers at 26% or 14%. BBH’s practitioner framework (Justin Reed, April 30, 2025) recommends ±25% relative bands at the sub-asset class level for taxable portfolios - this is the closest published guidance to leveraged ETF-specific thresholds, though it addresses standard equity sub-classes rather than 3x leveraged positions specifically.

For a 20-35% leveraged ETF allocation: Tighter bands of ±20% are appropriate given the larger absolute impact of drift on portfolio risk.

For allocations above 35%: Quarterly at minimum, with threshold monitoring between scheduled dates. At this allocation level, leverage drift meaningfully changes portfolio risk within a single quarter.

The asymmetry problem

Threshold rebalancing of a leveraged ETF creates an important asymmetry to understand. When TQQQ rises sharply and triggers a rebalance, you are selling a position that has been compounding favorably - potentially in the middle of a trend. When TQQQ falls sharply and triggers a rebalance on the downside, you are buying more of a position that may continue falling.

This is not a flaw in the strategy - it is the intended mechanism. Buying more TQQQ when it is down (as part of rebalancing) and trimming when it is up (as part of rebalancing) is a systematic way to maintain your risk budget regardless of emotional state. The 2022 experience is illustrative: investors who rebalanced into TQQQ in Q3 and Q4 2022 as it fell toward its December lows captured a significant portion of the 2023 recovery. Those who did not rebalance - either out of fear or inattention - held a smaller position when the recovery happened.

Tax Treatment: The Variable That Changes Everything

Rebalancing a leveraged ETF position in a taxable account creates taxable events. This is not a minor consideration - it is often the primary factor determining the practical rebalancing strategy.

In a taxable account (US investors)

Every sale of TQQQ or UPRO to rebalance crystallizes a capital gain. If the position has been held less than one year, the gain is taxed at ordinary income rates - up to 37% in the top US federal bracket. This tax cost must be weighed against the benefit of restored allocation.

Practical framework for taxable accounts:

Use new contributions to rebalance first. If you are adding $2,000/month to the portfolio, direct contributions to whichever asset class is underweight before triggering any sale. This avoids creating taxable events entirely while contributions are sufficient to correct drift.

Use threshold bands wide enough to avoid frequent rebalancing. In a taxable account, many practitioners widen bands to ±30-35% relative to avoid the tax drag of frequent small rebalancing events.

Tax-loss harvest the rebalancing opportunity. When TQQQ falls significantly and triggers a downside rebalance, sell the position, buy a non-substantially-identical fund for 31 days, then return to TQQQ. This captures a tax loss that offsets other gains while maintaining the rebalancing discipline.

In a tax-advantaged account (Roth IRA, ISA, pension)

Rebalancing inside a tax-advantaged account eliminates all tax considerations from the rebalancing decision. You can rebalance as frequently as the threshold triggers warrant, without any tax cost.

This is one of the strongest arguments for holding the leveraged ETF position inside a Roth IRA or equivalent tax-sheltered account. Beyond avoiding the tax drag on distributions and the financing cost embedded in daily resets, it also removes the tax friction from necessary rebalancing - allowing the threshold strategy to operate without the additional variable of crystallized gains.

Rebalancing Frequency: What the Research Actually Shows

The QuantPedia research - Margareta Pauchlyova, “Leveraged ETFs in Asset Allocation: Opportunity or Trap?” Quantpedia, November 16, 2025 (quantpedia.com/leveraged-etfs-in-asset-allocation-opportunity-or-trap/) - examined leveraged ETF allocation strategies across 1926-2025 using simulated and actual LETF data. Key findings:

- Static allocations with no rebalancing consistently underperformed threshold-based approaches over full market cycles

- Monthly rebalancing generated higher transaction costs than quarterly or threshold-based approaches without proportional improvement in risk-adjusted returns

- Trend-following signals applied to rebalancing frequency - reducing leveraged exposure after confirmed downtrends - materially improved drawdown outcomes

The Vanguard research (Zhang, Ahluwalia, Daga, Zi - “The Rebalancing Edge,” December 2024) quantified the benefit of threshold-based rebalancing for a 60/40 portfolio: threshold-based approaches generated 15-22 basis points of additional annual return versus monthly rebalancing, and 5-8 basis points versus quarterly rebalancing, primarily through reduced unnecessary transaction costs. For portfolios containing high-volatility leveraged ETFs, the drift risk from annual calendar rebalancing is amplified relative to a standard 60/40 - making the case for threshold-based approaches stronger, not weaker.

| Rebalancing Approach | Transaction Frequency | Tax Efficiency | Drift Risk vs. Target |

|---|---|---|---|

| Monthly calendar | High | Poor | Low (but over-trades) |

| Quarterly calendar | Moderate | Moderate | Moderate - TQQQ can move 30%+ between dates |

| Annual calendar | Low | Good | High - allocation can drift 10+ percentage points in a bull year |

| Threshold ±25% relative | Event-driven | Good | Controlled by design |

| Contribution-first + threshold | Lowest | Best | Controlled, zero tax events while contributions suffice |

Vanguard (December 2024) quantified threshold vs. quarterly at 5-8 bps annual benefit for a standard 60/40. The benefit is higher for portfolios containing leveraged ETFs due to faster and larger allocation drift.

The HFEA Case Study: What Quarterly Rebalancing Produced

The 55/45 UPRO/TMF strategy (HFEA) used quarterly rebalancing as its baseline. The 2022 experience stress-tested that approach under extreme conditions.

A real-world HFEA investor who began the strategy in November 2021 reported -59.50% YTD return by May 2022 - with quarterly rebalancing in place throughout. By the end of 2022, the full-year loss for the standard 55/45 quarterly-rebalanced HFEA portfolio was approximately -65%. UPRO fell -57.2% in 2022. TMF fell approximately -75% before its 1-for-10 reverse split.

In Q1 2022: both UPRO and TMF fell. The relative allocation barely changed, so quarterly rebalancing triggered minimal activity.

In Q2 and Q3 2022: both continued falling simultaneously. The TMF position - the supposed negative-correlation hedge - was falling faster than UPRO. Quarterly rebalancing meant systematically buying more TMF each quarter at progressively lower prices, into a structural headwind (rising rates) that showed no sign of reversing.

Investors who modified the rebalancing rule - switching to a threshold approach with a lower TMF target, or holding cash when TMF breached a lower band - reduced their 2022 losses relative to fixed quarterly rebalancing. No published backtest provides a precise verified comparison between threshold and quarterly rebalancing for the specific 55/45 HFEA portfolio in 2022. What is verifiable: the standard quarterly-rebalanced strategy lost approximately -65% in 2022, and $10,000 invested in HFEA on January 1, 2023 grew to $14,751 by June 30, 2024 - a 47.51% recovery that barely exceeded the S&P 500’s 45.40% over the same period. The mechanism is documented even where the exact differential is not: not being forced to systematically buy more of the worst-performing component on a fixed calendar schedule reduces the compounding of losses in a sustained structural drawdown.

The lesson is precise: rigid quarterly rebalancing into a position with a broken structural premise (TMF in rising-rate conditions) amplified losses. Threshold bands with the option to hold cash rather than rebalance into a deteriorating position is more robust - not because thresholds are magic, but because they respond to actual drift rather than assuming the allocation is always worth restoring.

Rebalancing in Practice: A Step-by-Step Framework

Step 1: Set your target allocation and thresholds before you invest. Define the leveraged ETF allocation (e.g., 20% TQQQ), the threshold trigger (e.g., ±25% relative, meaning rebalance at 25% or 15%), and the account type (taxable or tax-advantaged). Write it down. This decision is made when calm, not when TQQQ is up 40% or down 50%.

Step 2: Use new contributions to rebalance first. Every contribution goes to whichever position is furthest below its target. This delays the threshold trigger and avoids taxable events. In a taxable account, this is the most tax-efficient rebalancing mechanism available.

Step 3: Check allocation monthly, act on threshold. A monthly calendar check is not the same as monthly rebalancing. Check whether the allocation has breached the threshold. If it has, rebalance. If it has not, do nothing. The check takes five minutes. Most months, no action is required.

Step 4: For downside triggers in a taxable account, evaluate tax-loss harvesting. If TQQQ has fallen enough to trigger the lower threshold (e.g., from 20% to 14%), consider whether the position has also fallen enough to harvest a tax loss. Sell TQQQ, hold SOXL or another non-substantially-identical fund for 31 days, then return. You capture the tax loss and complete the rebalancing objective simultaneously.

Step 5: After a major bull run, trim systematically. When TQQQ has grown from 20% to 28% and triggers the upper threshold, sell the excess. This is the hardest rebalancing action psychologically - selling a position that has been performing well. The investor from the opening of this guide - who watched TQQQ drift from 20% to 26.2% through 2021 without acting - is the precise example of what happens when this step is skipped. That 6% of extra exposure cost $10,980 in additional 2022 losses. The trim in late 2021, had it happened, would have cost one transaction and a small taxable gain. The failure to trim cost far more.

For Non-US Investors

The rebalancing framework applies globally. What changes is the tax treatment of rebalancing events - and those differences are significant enough to affect practical strategy.

Israeli Investors

Israeli residents pay 25% capital gains tax on the real (inflation-adjusted) gain from the sale of securities, per the Income Tax Ordinance. As of 2025, investors whose annual capital income exceeds NIS 721,560 face an additional 2% surtax on top of the existing 3% general income surtax - bringing the effective rate on high-income capital gains to 30% above that threshold. Capital losses can be offset against capital gains, dividend income, and interest from other securities (provided the income was not taxed above 25%), and can be carried forward indefinitely.

What this means in practice for a TQQQ portfolio:

Consider an Israeli investor with a $300,000 portfolio, 20% TQQQ ($60,000), who holds through a strong bull run and TQQQ reaches 27% of the portfolio ($81,000 - a gain of $21,000 at 35% portfolio growth). Selling $20,100 of TQQQ to rebalance back to 20% crystallizes a gain of roughly $7,000 (assuming the position was up 35%). At 25% CGT, the tax cost is approximately $1,750 - before considering whether the threshold was worth triggering or whether new contributions could have handled the drift instead.

This is exactly why the contribution-first rule matters more for Israeli investors than for US investors in tax-advantaged accounts. Every NIS 100 of rebalancing gain avoided through contribution redirection saves NIS 25 in tax. For portfolios with regular contributions, most drift can be corrected without any sale.

Tax-loss harvesting in Israel: When TQQQ falls and triggers the lower threshold, Israeli investors face the same opportunity as US investors: sell to realize the loss, hold a different instrument for 31 days to avoid the wash-sale equivalent concern under Israeli tax practice (the Israeli Tax Authority has not issued a formal wash-sale rule identical to the US one, but best practice is to maintain a different instrument for 30+ days), then return to TQQQ. Realized losses carry forward indefinitely and offset future capital gains at the 25% rate.

New immigrant (oleh) exemption: Israeli residents who qualify as new immigrants (olim hadashim) are exempt from Israeli tax on foreign-source capital gains for 10 years from the date of aliyah. For an oleh investing in US-listed leveraged ETFs through an overseas broker, rebalancing transactions during the exemption period generate zero Israeli tax liability. This is a significant practical advantage - rebalancing can follow the optimal threshold framework without any tax friction during the exemption window.

EU Investors (UCITS Leveraged ETFs)

EU investors holding 2x UCITS leveraged ETFs rather than 3x US products face the same rebalancing framework with narrower threshold bands appropriate to the lower volatility profile of 2x leverage. German investors at 25% Abgeltungsteuer and UK investors at 18-24% CGT face similar contribution-first logic: direct new capital to underweight positions before triggering sales.

IBKR Tools for Non-US Investors

Interactive Brokers’ portfolio analyst tools allow threshold monitoring across accounts. Non-US investors using IBKR can set allocation alerts that trigger when positions breach defined bands - automating the monthly check step without requiring manual calculation.

Common Rebalancing Mistakes

Setting bands too tight in a taxable account. A ±10% relative threshold on a 20% TQQQ allocation means rebalancing every time the position moves from 20% to 22%. In a year like 2023 (+198% for TQQQ), this triggers multiple taxable events and short-term gains that erode the compounding benefit.

Rebalancing emotionally instead of mechanically. The threshold exists precisely to remove discretion. If you deviate from the threshold because “TQQQ looks like it will keep going up” or “the market seems uncertain,” you have abandoned the system. The 2021 investors who skipped trimming their overweight TQQQ position made this exact mistake.

Ignoring the lower threshold. Most investors are diligent about trimming when leveraged ETFs rally. Few are as disciplined about buying back when they fall. The lower threshold matters as much as the upper one - it is how the strategy systematically buys after declines rather than selling into them.

Forgetting the tax year. In a taxable account, rebalancing in December versus January can shift significant gains from one tax year to the next. For large positions, the timing of the rebalancing event matters for annual tax planning.

Using calendar rebalancing for a portfolio with high-VIX exposure. In periods when the VIX is above 25 and leveraged ETFs are moving 10-15% per week, a quarterly calendar rebalance means the allocation can drift dramatically between scheduled dates. Threshold monitoring is essential during high-volatility periods.

Frequently Asked Questions

Does rebalancing more frequently reduce volatility decay? No. Volatility decay is a function of the daily variance of the underlying index multiplied by the leverage factor. It operates inside the fund regardless of how often you rebalance your allocation to it. Rebalancing frequency controls concentration risk and allocation drift - it does not affect the fund’s internal decay mechanism.

Should I rebalance monthly or quarterly? Neither as a calendar rule. Threshold-based rebalancing - acting when the allocation drifts beyond a defined band - consistently outperforms calendar approaches in risk-adjusted return terms. Use calendar monitoring (monthly check) with threshold-based action.

What threshold bands should I use for TQQQ at 20% allocation? A ±25% relative band (rebalance at 25% or 15%) is appropriate for a taxable account. A ±20% relative band (rebalance at 24% or 16%) is appropriate for a tax-advantaged account where transaction costs are lower.

How do I rebalance without triggering large taxable gains? Use new contributions to rebalance first. Direct all new capital to underweight positions before triggering any sale. In a year with large contributions relative to portfolio size, this can handle most drift without any taxable event.

Is rebalancing into TQQQ after a large decline a good idea? Mechanically, yes - if it brings your allocation back to target, it is the right action under the threshold framework. Emotionally, it is the hardest rebalancing action to execute. This is exactly why the threshold is set in advance: to remove the discretion that would otherwise cause you to avoid buying after a decline.

Final Verdict

Rebalancing a portfolio that contains leveraged ETFs requires one framework adjustment from standard portfolio management: threshold-based triggers rather than calendar schedules, because high-volatility positions drift faster and further than calendar assumptions account for.

Beyond that adjustment, the principles are the same as any disciplined rebalancing approach. Set the allocation before you invest. Use contributions before sales. Act on the threshold, not on opinion. In a taxable account, harvest losses when the downside threshold triggers. In a tax-advantaged account, rebalance without restriction.

The investors who managed leveraged ETF allocations successfully through 2022 - one of the worst years in TQQQ’s history - did two things: they held small enough positions that the drawdown did not force a sale, and they had a written rebalancing rule they followed when it triggered. The rule replaced the judgment call that would have led most investors to either do nothing or sell at the bottom.

Write the rule before you need it. Follow it when you do.

For a deeper understanding of why volatility decay occurs mathematically - and four strategies that address it at the product and portfolio level - see our companion guide: Volatility Decay in Leveraged ETFs: The Math, the Myth, and Four Strategies That Actually Work.

This article is for informational and educational purposes only. It does not constitute financial, tax, or investment advice. Leveraged ETFs involve substantial risk of loss, including the possibility of losing the entire invested amount. Tax rules cited reflect publicly available guidance as of May 2026 and may change; Israeli and international investors should verify current tax treatment with a qualified local tax advisor before executing any rebalancing strategy. Past performance of any leveraged ETF strategy is not indicative of future results.