Important: This guide covers advanced options strategies on a 3x leveraged ETF. Both components carry significant risk individually. Combined, the risks multiply. This article is educational, not financial advice. Read the risk sections in full before considering any trade.

The core idea is simple. TQQQ is one of the most volatile ETFs in existence. Volatility is what options traders sell. Put those two facts together and you get one of the richest premium environments available to individual investors - a leveraged ETF that generates option income at roughly three times the rate of its non-leveraged equivalent.

The execution is not simple. Selling options on TQQQ without understanding implied volatility, the Greeks, and what happens when a position moves against you is how traders generate large losses while believing they are generating income. This guide covers the full picture - the mechanics, the numbers, the risks, and the specific decisions you face when the market does not cooperate.

As of late May 2026, TQQQ is trading at approximately $72-75 per share. All examples use $75 as the reference price. Premiums are calculated using Black-Scholes with 60% IV and 30 DTE, and cross-referenced against current options chain data.

Meet Ryan

Ryan is 44, lives in Austin, holds 200 shares of TQQQ worth approximately $15,000, and has $8,000 in cash sitting in his brokerage account earning 4.1%. He has read about covered calls and cash-secured puts and wants to understand whether combining them into a systematic income strategy makes sense on TQQQ specifically.

He is not a beginner. He has traded options on individual stocks. But TQQQ is a different animal and he knows it - which is why he is reading this before placing any trade.

One more thing about Ryan: his brokerage account holds $22,000 in total - below the $25,000 Pattern Day Trader threshold. This matters for how he manages positions, and we will return to it.

We will follow Ryan through every decision in this guide.

Part One: Why TQQQ’s Implied Volatility Is the Heart of This Strategy

Before touching the mechanics of any specific trade, you need to understand implied volatility - because on TQQQ, IV is not just a pricing input. It is the primary reason the strategy generates the income it does.

TQQQ targets three times the Nasdaq-100’s daily return and resets that leverage every trading day. In a sustained trend, daily compounding can amplify gains; in a choppy market, the same reset creates volatility decay. If QQQ rises 10% and then falls 10%, it finishes down 1%, while an approximate 3x sequence leaves TQQQ down about 9%. Covered-call and cash-secured-put income sits on top of that path-dependent underlying behavior.

What Implied Volatility Actually Measures

Implied volatility (IV) is the market’s expectation of how much an asset will move over a given period, expressed as an annualized percentage. It is derived mathematically from current option prices - working backwards from what the market is paying for options to infer the volatility those prices imply.

When an option on TQQQ costs more, IV is higher. When it costs less, IV is lower. IV is not a prediction of direction - it is a measure of expected magnitude of movement, in either direction.

TQQQ’s IV versus QQQ’s IV - the critical comparison:

As of late May 2026, TQQQ’s 30-day implied volatility runs approximately 55-60%, with an IV percentile around 60% (Option Samurai, April 2026). QQQ’s 30-day IV runs approximately 18-22% under the same market conditions - roughly three times lower.

This gap is not accidental. TQQQ seeks to deliver 3x the daily return of QQQ. Its realized volatility is approximately three times QQQ’s realized volatility. The options market prices that in precisely. A 1% move in QQQ becomes approximately a 3% move in TQQQ - and options on TQQQ are priced to reflect that range of outcomes.

What this means in dollars: A 30-day at-the-money call on QQQ generates roughly 1.5-2% of the underlying’s price in premium. The same call on TQQQ at equivalent moneyness generates approximately 5-8%. That differential is real income - and it is the primary reason traders use TQQQ as an options underlier.

What this means for risk: The premium is three times richer because the risk is three times higher. TQQQ can move 10-15% in a week during volatile market conditions. Options priced for that range are not mispriced. Every dollar of premium collected on TQQQ is compensation for accepting that range of outcomes.

IV Rank and IV Percentile - Reading the Signal

Two metrics tell you whether current IV is high or low relative to history:

IV Rank (IVR): Where current IV sits within the 52-week high-to-low range. IVR of 70 means current IV is in the top 30% of its annual range.

IV Percentile (IVP): The percentage of days in the past year where IV was lower than today. IVP of 60 means IV has been lower on 60% of trading days this year.

For premium sellers, both metrics matter. Selling options when IV is elevated (IVR above 50, IVP above 50) means collecting richer premiums and benefiting from IV mean-reversion - the tendency of elevated IV to compress back toward its average as fear subsides. Selling when IV is low means collecting thin premiums while accepting the same underlying risk.

Ryan checks IV before every trade. Not obsessively - once per week is sufficient for monthly positions. He targets entering new positions when TQQQ’s IVR is above 40.

Part Two: The Greeks You Cannot Ignore

Options traders use the Greeks to measure how a position’s value changes as conditions change. On TQQQ, three Greeks dominate every decision.

Delta: Your Directional Exposure

Delta measures how much an option’s price changes for every $1 move in TQQQ. An at-the-money option has a delta of approximately 0.50 - it moves $0.50 for every $1 the underlying moves. A 10% OTM option might have a delta of 0.20-0.30.

As a call seller, your delta exposure is negative - you benefit when TQQQ falls or stays flat, and lose when it rises sharply. As a put seller, your delta exposure is positive - you benefit when TQQQ rises or stays flat, and lose when it falls.

Why delta matters more on TQQQ: Because TQQQ moves approximately 3x the Nasdaq-100, a 2% index move translates to roughly 6% in TQQQ. On a $75 position, that is $4.50 per share in a single session. If your short call has a delta of 0.25 and TQQQ moves $4.50 against you, your option moves approximately $1.12 against you - in hours, not days. Delta management on TQQQ requires more attention than on slower-moving underlyings.

Strike selection and delta: Most experienced TQQQ options sellers target short options with a delta between 0.20 and 0.35 - roughly 7-15% out of the money. This gives enough buffer to absorb normal TQQQ volatility while collecting meaningful premium. ATM options (delta ~0.50) generate maximum premium but leave almost no room for the underlying to move before the position is challenged.

Theta: The Decay That Works in Your Favor

Theta measures how much an option loses in value each day due to time passage alone, holding everything else constant. As an option seller, theta works in your favor - every day that passes without a large adverse move, your short option decays and you profit.

TQQQ options have high theta in absolute dollar terms, directly reflecting elevated IV. A 30-day ATM call on TQQQ might carry a theta of $0.12-0.18 per day - meaning the option loses that value daily purely from time passage. On a 100-share contract, that is $12-18 of daily decay in your favor.

Theta accelerates as expiration approaches: options lose roughly one-third of remaining time value in the final week and two-thirds in the final two weeks. The standard range of 21-45 days to expiration captures the steepest part of this decay curve while still allowing time to manage positions that move against you.

Vega: The Risk That Blindsides Premium Sellers

Vega measures sensitivity to changes in implied volatility. As a premium seller, you are short vega - rising IV hurts you, falling IV helps you.

On TQQQ this creates an important asymmetry. When TQQQ falls sharply - a bad macro week, a Fed decision, a Nasdaq selloff - implied volatility typically spikes simultaneously. The option you sold becomes worth more not just because of delta (the price moved against you) but also because of vega (IV expanded and made the option more expensive). This double effect - delta loss plus vega expansion - is why short premium positions on TQQQ can lose faster than traders expect during market dislocations.

Ryan understands this dynamic. In a sharp TQQQ selloff, his short put position faces both delta and vega headwinds simultaneously. He sizes every position to withstand this combined effect - not just the directional move alone.

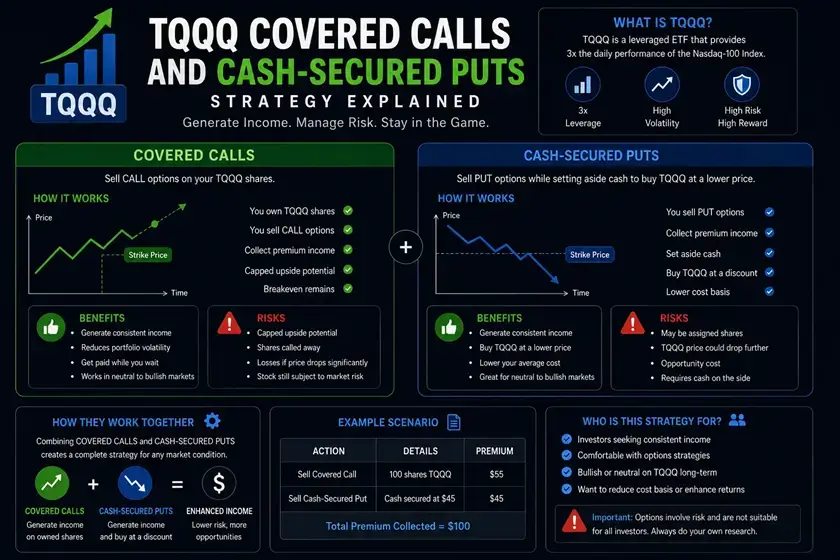

Part Three: Covered Calls on TQQQ - Real Numbers

Ryan owns 200 TQQQ shares at $75 per share ($15,000). He sells one covered call against 100 shares, keeping 100 shares uncovered to preserve meaningful upside exposure on half his position.

The Mechanics and Correct Premiums

Example trade - June 2026 expiration, 30 DTE, IV 60%:

Using Black-Scholes pricing (S=$75, IV=60%, r=4.5%, 30 DTE, no dividend):

- Strike $82 (9.3% OTM, delta ~0.25): Theoretical premium approximately $3.80-4.20

- Strike $85 (13.3% OTM, delta ~0.18): Theoretical premium approximately $2.80-3.20

- Strike $78 (4% OTM, delta ~0.38): Theoretical premium approximately $5.50-6.00

Ryan selects the $82 strike at approximately $4.00 per share ($400 per contract).

- Return on position: 5.3% over 30 days on the 100 shares covered

- Maximum gain if called away: $82 strike + $4 premium - $75 cost = $11 per share ($1,100)

- Downside buffer: the $400 premium reduces effective cost basis to $71, providing a 5.3% buffer

Three outcomes at expiration:

TQQQ stays below $82: The call expires worthless. Ryan keeps the $400. He sells another call for the following month. On an annualized basis, consistent execution at this level would generate approximately 48-60% of his position value in gross premium - before tax and before accounting for positions that do not go as planned.

TQQQ rises above $82: His 100 shares are called at $82. Total proceeds: $8,200 (shares) + $400 (premium) = $8,600 on a $7,500 investment - a 14.7% gain in 30 days. He misses any move above $82 on those 100 shares. His uncovered 100 shares fully participate in the rally.

TQQQ falls significantly: The call expires worthless (Ryan keeps the $400), but his shares are worth less. If TQQQ falls 20%, the covered shares decline from $7,500 to $6,000. The premium reduces the $1,500 underlying loss to $1,100, but Ryan still loses 14.7% on the covered position despite completing a profitable option trade. Premium is a buffer, not protection against a leveraged drawdown.

The Upside Cap Problem - Why Ryan Only Covers Half

TQQQ is held precisely because of its potential for explosive returns. On April 9, 2025, TQQQ gained 35.2% in a single day. An investor who had covered 100% of their position that day would have captured only the premium plus appreciation to their strike - potentially missing 25-30% of that day’s move.

Systematically selling covered calls on 100% of a TQQQ position means systematically selling the outcome that makes holding TQQQ worthwhile. Ryan’s solution: cover half, leave half unencumbered. The covered half generates monthly income. The uncovered half participates fully in any large moves.

A Realistic Monthly Income Scenario

The same covered-call position produces very different results across market regimes. In a calm, moderately bullish month, Ryan may keep the full $400 premium while his shares appreciate below the strike. In a volatile but flat month, higher IV can increase the premium while the shares finish near their starting value. In a bad month, a 20-25% TQQQ decline can overwhelm several months of collected premium at once.

This is why Ryan evaluates income against total position return rather than counting premium in isolation. A successful expiration does not make the month profitable if the underlying loss is larger, and the covered-call allocation must be small enough that one leveraged drawdown does not damage the broader account.

Part Four: Cash-Secured Puts on TQQQ - Real Numbers

Ryan has $8,000 in cash. He sells cash-secured puts to get paid while waiting for a better entry to buy more TQQQ.

The Mechanics and Correct Premiums

Example trade - June 2026 expiration, 30 DTE, IV 60%:

Using Black-Scholes (S=$75, IV=60%, r=4.5%, 30 DTE):

- Strike $68 (9.3% OTM, delta ~-0.25): Theoretical premium approximately $3.50-4.00

- Strike $65 (13.3% OTM, delta ~-0.18): Theoretical premium approximately $2.50-3.00

- Strike $71 (5.3% OTM, delta ~-0.35): Theoretical premium approximately $5.00-5.50

Ryan selects the $68 strike at approximately $3.80 per share ($380 per contract).

- Cash required as collateral: $6,800 ($68 × 100 shares)

- Effective purchase price if assigned: $68 - $3.80 = $64.20 per share

- Break-even: TQQQ must fall below $64.20 for Ryan to lose money on the combined position

- Return if not assigned: $380 / $6,800 = 5.6% in 30 days

Three outcomes at expiration:

TQQQ stays above $68: The put expires worthless. Ryan keeps $380. His $6,800 in collateral is released. He sells another put. In 30 days he earned 5.6% on capital that was previously earning 4.1% annually.

TQQQ falls to $68: The put may be assigned. Ryan buys 100 shares at $68, effective cost $64.20 - a 14.4% discount to the price when he sold the put. He has acquired more TQQQ at a meaningful discount, with a lower cost basis than simply buying the dip directly.

TQQQ falls sharply below $64: Ryan is assigned at $68, effective cost $64.20, but TQQQ is trading at $55 or lower. The $380 premium offsets a fraction of the paper loss. This is the real risk - being obligated to buy a 3x leveraged instrument at a price substantially above where it is currently trading, in a market that may fall further.

Ryan only sells puts in quantities he is financially and psychologically able to hold at the assignment price through a severe drawdown. He does not view assignment as a disaster - but he sizes positions so that even full assignment on a position that then falls 40% does not force him to sell.

Part Five: The Wheel Strategy - Connecting the Two

The Wheel Strategy combines cash-secured puts and covered calls into a continuous cycle: sell puts, get assigned, sell covered calls against the assigned shares, get called away, sell puts again. At every phase, premium is collected regardless of market direction.

The Full Cycle with Ryan’s Numbers

Month 1 - Phase 1 (Cash-Secured Put):

- Sell the $68 put for $380 premium

- TQQQ falls to $65 - Ryan is assigned at $68

- Effective cost basis: $64.20 after premium

Month 2 - Phase 2 (Covered Call):

- TQQQ is at $66. Ryan sells the $70 covered call for approximately $3.50 ($350 premium)

- New effective cost basis: $64.20 - $3.50 = $60.70

- TQQQ recovers to $71 - shares called away at $70

- Net result: sold at $70, cost basis $60.70, capital gain $9.30 per share ($930) plus $730 in premiums across two months

If the wheel completes cleanly: Ryan collected $730 in premium across two months and locked in $930 in capital gain - $1,660 total return on $6,800 in capital over 60 days. This is the best-case scenario. It is also the scenario that fills Reddit threads.

If the wheel breaks down: TQQQ falls to $50 after Ryan is assigned at $68. His 100 shares are worth $5,000. He sells covered calls at $55 to collect premium - approximately $2.50-3.50 per month on a position that needs a 36% recovery just to reach his assignment price. The premium income helps but does not meaningfully accelerate recovery from a large drawdown on a 3x leveraged instrument.

The 2022 Case Study - What Actually Happened to Wheel Traders

The Wheel Strategy on TQQQ faced its most significant real-world test in 2022. TQQQ fell from approximately $91 in late 2021 to approximately $16 by December 2022 - an 82% peak-to-trough decline.

It is important to be precise about what this meant for a Wheel trader, because the narrative is often stated inaccurately. An investor who ran cash-secured puts throughout 2022 was not sitting on an 82% loss. They were being assigned TQQQ at progressively lower prices - $80, $70, $60, $50, $40, $30 - each time with a lower effective cost basis due to accumulated premium. Their blended cost basis across all assignments was substantially above the $16 trough, but also substantially below the $91 starting price.

The actual experience: repeated assignments locked increasing amounts of capital into a falling instrument. Covered calls sold against assigned positions collected premium - at the elevated IV of a bear market, actually generous premium - but could not be set above cost basis without immediate exercise at a loss. The strategy was not generating losses from premium collection; it was generating losses from owning an instrument that fell 82%.

Recovery required TQQQ to return to or above each investor’s blended cost basis - not necessarily the full +476% from the $16 trough. An investor assigned at an average of $45 across 2022 needed approximately a +180% recovery to break even, not +476%. TQQQ delivered that recovery by mid-2024.

The lesson: the Wheel on TQQQ in a bear market converts what would have been a single large loss into a series of smaller, staged entries at progressively lower prices - which is actually a form of involuntary DCA. The problem is capital commitment: each assignment requires more cash or margin, and the total capital locked in the strategy grows as TQQQ falls. Investors who ran out of capital to commit to new assignments were forced to hold existing positions without the income offset of new put premium. Those who maintained sufficient reserves and continued the cycle were rewarded in the 2023-2024 recovery.

Ryan’s rule: never run the Wheel on TQQQ with more capital than he can lock up for three years if needed, and always maintain a reserve that allows at least two additional assignment cycles beyond the current position.

Part Six: Rolling - What to Do When a Position Moves Against You

Rolling is closing an existing option position and simultaneously opening a new one with a different strike, expiration, or both.

Rolling a Covered Call

Scenario: Ryan sold the $82 call for $4.00 with 30 DTE. TQQQ rallied to $85 with 10 days remaining. His call is now ITM by $3. The call is worth approximately $6.00 - a $2.00 loss from his $4.00 sale.

Option A - Accept assignment. His 100 shares are called at $82. Total proceeds: $8,200 + $400 premium collected = $8,600 on a $7,500 investment. Solid return. He redeploys capital.

Option B - Roll up and out. He buys back the $82 call at $6.00 and simultaneously sells the $90 call expiring 30 days further out for approximately $4.50. Net debit on the roll: $1.50. He has extended his position 30 days and raised the ceiling to $90 - but paid $150 to do so.

Ryan’s rule on rolling: He rolls only for a net credit. If rolling the call requires paying a net debit, he accepts assignment. Paying to extend a position that has moved significantly against you compounds the problem without solving it. The one exception: if the net debit is very small ($0.20-0.30) and the new strike meaningfully raises his ceiling, the math may justify it.

Rolling a Cash-Secured Put

Scenario: Ryan sold the $68 put for $3.80 with 30 DTE. TQQQ fell to $64 with two weeks remaining. His put is now ITM.

Option A - Accept assignment. He buys 100 shares at $68, effective cost $64.20. He transitions to Phase 2 of the Wheel: selling covered calls.

Option B - Roll down and out. He buys back the $68 put (now worth approximately $6.50) and sells the $63 put expiring 30 days further out for approximately $4.00. Net debit: $2.50. He has lowered his assignment price to $63 but paid $250 to delay the assignment.

For TQQQ put rolls, accepting assignment and transitioning to covered calls is usually cleaner than rolling down. Rolling extends duration on a position moving against you while paying for the privilege. Unless Ryan has a specific, time-limited reason to believe TQQQ will recover quickly, the transition to covered calls is the more efficient path.

Part Seven: The PDT Rule - Critical for Accounts Under $25,000

This section is included because it is genuinely important and frequently omitted from options strategy guides.

The Pattern Day Trader (PDT) rule, enforced by FINRA for US brokerage accounts, defines a pattern day trader as anyone who executes four or more day trades within five business days in a margin account, where those trades represent more than 6% of total trades during that period. Accounts flagged as PDT must maintain a minimum equity of $25,000. Fall below $25,000 and the account is restricted from day trading until the balance is restored.

How this affects TQQQ options sellers:

Rolling an options position - buying back the existing option and selling a new one on the same day - counts as two trades but is generally not a day trade because you are not buying and selling the same security. Most standard rolls do not trigger PDT.

However, rapidly opening and closing positions in TQQQ shares - for example, buying shares after assignment and immediately selling covered calls, then having those calls exercised and immediately re-entering - can accumulate trades quickly in smaller accounts.

Ryan’s account holds $22,000. He manages this by using a cash account rather than a margin account for his TQQQ options positions. Cash accounts are not subject to the PDT rule - but they require full cash settlement before capital can be redeployed, which takes two business days (T+2) for equity options. He cannot immediately redeploy assignment proceeds into a new cash-secured put the same day.

For accounts under $25,000: Use a cash account for options strategies to avoid PDT restrictions. Accept the T+2 settlement delay as a structural limitation. Size positions so that natural settlement cycles do not create gaps in your income generation schedule.

For accounts over $25,000: The PDT rule is not a constraint, but maintaining a buffer above $25,000 is important - a few losing months on TQQQ options can push an account below the threshold and trigger restrictions at the worst possible time.

Part Eight: Early Assignment Risk

TQQQ options are American-style, meaning the buyer can exercise at any time before expiration - not just on the expiration date. Early assignment on standard options is rare when significant time value remains, because exercising early throws away that remaining time value. A rational buyer with a call worth $6.00 will not exercise early if intrinsic value is $4.00 and they could sell for $6.00 instead.

However, two situations increase early assignment probability:

Deep ITM calls approaching expiration: When a covered call is deep in-the-money and time value has nearly eroded - typically in the final 5-7 trading days - the bid-ask spread on the option can widen enough that selling the option is less attractive than simply exercising it. Ryan monitors any ITM call with fewer than 7 days to expiration and treats early assignment as probable rather than possible.

Deep ITM puts in fast-moving markets: Similarly, a deep ITM put in a rapidly falling market may be exercised early if the put buyer wants to lock in their gains immediately rather than waiting for expiration. This is less common but worth monitoring.

Ryan’s management rule: any option more than 5% ITM with fewer than 7 days to expiration is either rolled or accepted as likely to be assigned before expiration.

Part Nine: Tax Implications - The Full Picture

US Investors

Option premium income from expired or closed covered calls and cash-secured puts is classified as short-term capital gain, taxed at ordinary income rates regardless of how long you held the underlying TQQQ shares. For a US investor in the 24% marginal bracket, $400 in monthly premium generates $96 in federal tax. Net monthly income: $304. This is the number that matters for planning, not the gross premium.

Qualified covered call rules (IRS Publication 550): A covered call is “qualified” - meaning it does not interrupt the holding period of the underlying shares - only if the strike meets specific IRS guidelines. Deep ITM calls are generally non-qualified and may terminate the long-term capital gains holding period of TQQQ shares held for over a year. For investors who have held TQQQ long-term and want to preserve long-term treatment on eventual share sales, maintaining OTM strikes and reasonable expiration windows is important.

Assignment events: When TQQQ shares are called away (covered call assigned) or when put-assigned shares are later sold, the gain or loss on the stock position is separate from the premium. The holding period of the shares determines short-term or long-term treatment. Premium from the call reduces your effective sale price; premium from the put reduces your effective purchase price.

Wash sale rule: If you sell TQQQ shares at a loss and buy substantially identical securities within 30 days before or after, the loss is disallowed. Options on TQQQ may also trigger wash sale complications - closing a put position at a loss and selling another TQQQ put within 30 days can implicate wash sale rules. Consult a CPA if you are generating frequent losses on TQQQ options.

Non-US Investors - A More Complete Picture

The three-line treatment in most guides is inadequate for a strategy that generates regular income. Here is what actually varies by jurisdiction.

Germany: Premium income from covered calls and cash-secured puts falls under Abgeltungsteuer at 26.375% effective rate. The Teilfreistellung (30% partial exemption) that applies to equity ETF gains does not apply to options premium - options income is taxed in full at 26.375%. Active options trading may be classified as trading income (Gewerbebetrieb) rather than capital income if frequency and systematic nature suggest a commercial activity - this triggers higher marginal rates and social contributions. German options traders running monthly programs should confirm their classification with a Steuerberater.

UK: Options premium is taxed under Capital Gains Tax rules. The annual CGT exemption (£3,000 for 2026/27) can shelter modest premium income. Above the exemption, standard CGT rates apply: 18% for basic rate taxpayers, 24% for higher rate taxpayers on investment gains. High-frequency options activity may be reclassified as trading income by HMRC and taxed at income tax rates.

Australia: Options premium is generally treated as assessable income in the year received, not capital gain, unless specifically meeting CGT asset criteria. This means it is taxed at marginal income tax rates (up to 47% including Medicare levy) rather than the discounted CGT rate available on assets held over 12 months. The 50% CGT discount does not apply to options premium.

Canada: Options premiums are generally treated as income from a business rather than capital gains when the strategy is systematic and frequent - as a monthly Wheel Strategy would be. This means full marginal tax rates apply (up to 53.5% in high-tax provinces) rather than the 50% capital gains inclusion rate.

Currency risk: TQQQ and its options settle in US dollars. An investor funding the account in AUD, GBP, ILS, or another currency experiences both the leveraged TQQQ move and the exchange-rate move. A 20% decline in TQQQ combined with a 5% adverse currency move produces an approximate 24% loss in home-currency terms before option premium, fees, and tax.

The universal principle: Before running a systematic monthly options strategy on TQQQ, confirm with a qualified tax advisor in your jurisdiction how premium income will be classified. The difference between capital gains treatment and income treatment can be 10-20 percentage points of effective tax rate - a meaningful drag on net returns.

Ryan runs a simple tracker: gross premium collected, estimated tax at 24%, net after-tax income. He does not mentally spend the gross premium.

When This Works and When It Fails

The traders most likely to use this strategy successfully are tactical rather than automatic. They wait for IV to be elevated relative to its recent range, keep the TQQQ options allocation to roughly 5-10% of the total account, manage challenged positions actively, and treat the strategy as speculative income rather than a core passive-income holding. Anyone unable to monitor positions during US market hours should size even more conservatively or avoid the strategy.

In sideways markets with elevated volatility, this strategy is genuinely powerful. TQQQ moves without large directional trends, IV stays elevated, premiums are rich, and options expire worthless consistently. The Wheel generates income at every phase and rarely requires difficult management decisions.

In prolonged bear markets, the strategy faces its hardest test. Repeated put assignments lock increasing amounts of capital into a falling instrument. The premium collected - often generous in high-IV bear markets - does not offset large drawdowns on the underlying position. The 2022 case study is the reference point: the Wheel did not generate losses from premium collection, but it committed capital to an instrument that fell 82% from peak to trough. Investors who maintained sufficient reserves to continue the cycle were rewarded in the 2023-2024 recovery. Those who ran out of capacity to absorb additional assignments were not.

In sharp, fast-moving markets - single-day moves of 10-15% - positions that seemed conservatively placed can breach overnight. The vega expansion that accompanies sharp moves makes buy-back more expensive. This is not a theoretical risk on TQQQ. It has happened multiple times.

In low-volatility bull markets, covered calls cap a rally that could have been held in full, and put premiums are thin on positions that never get assigned. The strategy underperforms simply holding TQQQ - which is the correct comparison for anyone who holds TQQQ primarily for its price appreciation potential.

Where Ryan Ends Up

After six months of running the combined strategy with disciplined position sizing:

His covered call program (100 of his 200 shares) generates an average $380 per month in net premium after accounting for one position where he rolled for a small debit. Total over six months: approximately $2,100 gross, $1,596 net after 24% tax.

His cash-secured put program ($6,800 committed) generates an average $350 per month with two assignment events that transitioned cleanly to covered calls. Total over six months: approximately $1,950 gross, $1,482 net after tax.

Combined net after-tax income: approximately $3,078 over six months on $22,800 in deployed capital - approximately 27% annualized net return from options premium alone ($3,078 × 2 ÷ $22,800).

He did not earn that return by accident. He checked IV before every entry, used a cash account to avoid PDT constraints, defined rolling rules before positions opened, and sized put assignments to what he could hold through a 40% drawdown without selling.

The strategy worked. Not because he picked perfect strikes. Because he understood every mechanism before placing the first trade and built a framework that kept decisions rational when markets were not.

*This article is for educational purposes only and does not constitute financial, investment, or tax advice. Options trading involves significant risk of loss and is not suitable for all investors. TQQQ price data from Yahoo Finance (May 2026). IV data from Option Samurai (April 2026). Premiums calculated using Black-Scholes model with S=$75, IV=60%, r=4.5%, 30 DTE, validated against published options chain data. Tax treatment based on IRS Publication 550 (US), HMRC guidance (UK), ATO guidance (Australia), and CRA guidance (Canada), current as of May 2026. Consult a qualified financial advisor and tax professional before implementing any options strategy.

Frequently Asked Questions

What is the difference between selling covered calls and cash-secured puts on TQQQ? A covered call is sold against shares you already own - you collect premium in exchange for capping your upside to the strike price. A cash-secured put is sold against cash you hold - you collect premium in exchange for agreeing to buy 100 shares at the strike price if TQQQ falls below it. Both generate income from TQQQ’s elevated implied volatility. The Wheel Strategy connects both into a continuous cycle: sell puts, accept assignment, sell covered calls, get called away, sell puts again. See the Wheel Strategy guide for a full walkthrough.

Why is TQQQ’s implied volatility so much higher than QQQ’s? Because TQQQ delivers 3x the daily return of QQQ, its realized volatility is approximately three times QQQ’s. Options markets price implied volatility to reflect expected realized volatility. TQQQ’s 30-day IV runs 55-60% versus 18-22% for QQQ - roughly a 3x ratio. This is why covered calls and puts on TQQQ generate approximately three times the premium of equivalent options on QQQ. The higher premium is compensation for higher risk, not a market inefficiency.

What premiums can I realistically expect on TQQQ options? At current IV levels (~60%), a 30-day covered call approximately 9% OTM (delta ~0.25) on TQQQ at $75 generates approximately $3.80-4.20 per share, or $380-420 per contract (Black-Scholes, confirmed against options chain data). A comparable cash-secured put generates $3.50-4.00 per share. These are gross premiums before tax. At 24% marginal rate (US), net premiums are approximately $2.90-3.20 per share for the call and $2.66-3.04 for the put.

What is the PDT rule and how does it affect TQQQ options traders? The Pattern Day Trader rule requires US margin accounts with fewer than $25,000 in equity to limit day trades to three per five-business-day period. Accounts below this threshold that exceed the limit are restricted. Options sellers running monthly Wheel strategies on TQQQ with accounts under $25,000 can avoid PDT restrictions by using a cash account instead of a margin account - cash accounts are not subject to PDT rules. The trade-off is T+2 settlement, meaning assignment proceeds cannot be immediately redeployed the same day.

When should I roll versus accepting assignment? Roll a covered call when: the position can be rolled for a net credit, and the new strike is genuinely above where you expect TQQQ to trade by the new expiration. Accept assignment when: rolling requires a net debit, or the position has moved so far ITM that extending it is chasing a losing battle. For cash-secured puts: accept assignment and transition to covered calls rather than rolling down for a net debit in most cases. The clean transition to Phase 2 of the Wheel is usually more efficient than paying to delay the inevitable.

How are TQQQ options premiums taxed outside the US? It varies significantly. In Germany, premium income is taxed at 26.375% (Abgeltungsteuer) with no partial exemption - systematic monthly programs may be reclassified as trading income at higher rates. In the UK, premiums fall under CGT at 18-24% above the annual exemption, but HMRC may reclassify frequent activity as trading income. In Australia, options premium is generally assessable income at marginal rates, not capital gain. In Canada, systematic options programs are typically treated as business income at full marginal rates. Confirm the classification with a qualified tax advisor in your jurisdiction before starting - the difference between capital gains and income treatment can be 10-20 percentage points of effective tax rate.